Accounting is often regarded as the language of business because it provides a structured method for recording, analyzing, and communicating financial data. The accounting cycle is a fundamental process that serves as the cornerstone of financial reporting for businesses and organizations. In this article, we will delve into the accounting cycle, its essential steps, and the significance of the accounting cycle.

What you are going to learn?

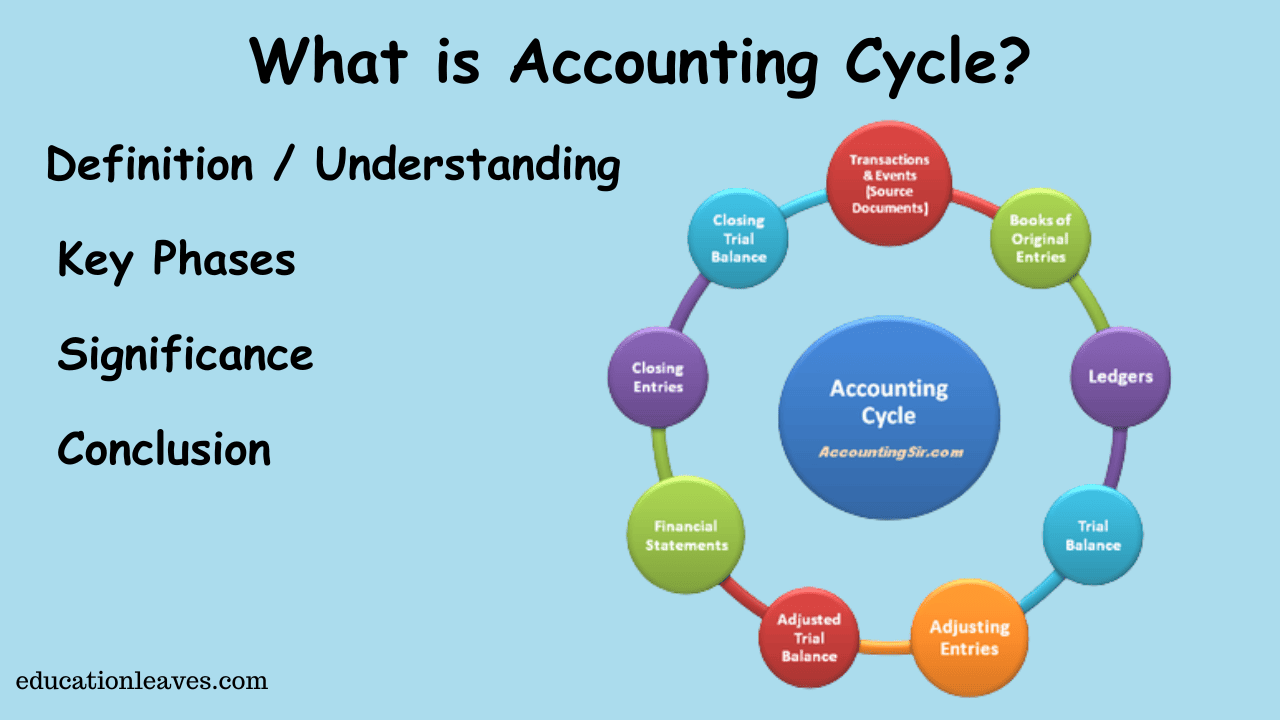

Understanding the Accounting Cycle

The accounting cycle comprises a sequence of well-defined and interconnected steps that accountants and financial professionals follow to record, process, and report financial transactions. It offers a systematic approach to ensure that financial data is accurately recorded and that financial statements, such as income statements and balance sheets, are prepared consistently and promptly.

The accounting cycle usually covers a specific period, such as a month, quarter, or fiscal year, depending on the reporting requirements of the entity.

Key Phases in the Accounting Cycle

1. Transaction Identification:

The initial step in the accounting cycle involves identifying and analyzing financial transactions. These transactions can encompass sales, purchases, investments, loans, and various other financial activities. Accountants must determine which accounts are affected by each transaction and whether it results in an increase or decrease in the account balances.

Example:

- On January 1st, ABC Electronics purchased $10,000 worth of electronic components on credit from a supplier.

- On January 5th, ABC Electronics sold $5,000 worth of electronic gadgets to a customer on credit.

- On January 15, ABC Electronics paid $2,000 to the supplier for the components purchased on January 1st.

- On January 20th, ABC Electronics received a $3,000 cash payment from the customer for the sale made on January 5th.

2. Transaction Recording:

Once transactions are identified, they are recorded in the accounting system using a double-entry accounting method. This means that every transaction affects at least two accounts, with one account debited (increased) and another account credited (decreased). This approach upholds the fundamental accounting equation: Assets = Liabilities + Equity.

Example: ABC Electronics records each of these transactions in its accounting journal. For example, on January 1st, it recorded a debit of $10,000 to the “Inventory” account and a credit of $10,000 to the “Accounts Payable” account.

3. Posting to the General Ledger:

Transaction data is subsequently posted to the general ledger, which serves as the primary accounting record containing all the accounts used by the entity. Each account in the ledger is updated with the appropriate information from the transactions.

Example: The information from the journal entries is then posted to the general ledger. In the ledger, each account has its own page where all transactions related to that account are recorded.

4. Trial Balance:

After all transactions are recorded and posted, a trial balance is prepared. This is a listing of all the ledger account balances, both debit and credit, designed to ensure that the accounting equation remains in equilibrium. Any discrepancies indicate errors in the recording process.

Example: At the end of the accounting period (usually a month), ABC Electronics compiles all the balances from the general ledger into a trial balance. This is a summary of all the debit and credit balances to ensure they are equal and the books are in balance.

5. Adjusting Entries:

Adjusting entries are introduced at the end of the accounting period to account for accrued revenues, expenses, and other items that may not have been recorded during the regular transaction recording. These entries guarantee that the financial statements accurately represent the company’s actual financial position.

Example: ABC Electronics reviews its accounts and makes any necessary adjusting entries. For example, it may recognize depreciation on its equipment or accrue for unpaid expenses.

6. Financial Statements:

Following the creation of adjusting entries, financial statements are prepared. The primary financial statements encompass the income statement, illustrating revenues and expenses, and the balance sheet, which presents the entity’s assets, liabilities, and equity.

Example: After adjusting entries are made, ABC Electronics prepares its financial statements, including the income statement, balance sheet, and cash flow statement. These statements provide a snapshot of the company’s financial performance and position.

7. Closing Entries:

At the conclusion of the accounting period, temporary accounts (such as revenue and expense accounts) are closed, meaning their balances are transferred to the retained earnings account on the balance sheet. This procedure resets these accounts to zero for the new accounting period.

Example: At the end of the accounting period, ABC Electronics closes temporary accounts such as revenue and expense accounts. This involves transferring their balances to the income summary account and then to the retained earnings account.

8. Post-Closing Trial Balance:

After closing entries are executed, a post-closing trial balance is compiled to verify that all temporary accounts have been appropriately closed and that the accounting equation remains in balance.

Example: After closing entries are made, a post-closing trial balance is prepared to ensure that all temporary accounts have been closed properly, and the books are ready for the next accounting period.

9. Reversing Entries (Optional):

Some businesses opt to employ reversing entries at the outset of the new accounting period to simplify the recording of specific transactions, particularly accruals. These entries reverse the effects of adjusting entries made at the end of the prior period.

Example: Some companies use reversing entries at the beginning of the new accounting period to simplify the recording of certain transactions, such as accruals.

Significance of the Accounting Cycle

The accounting cycle holds significant importance for the following reasons:

- Accuracy: It ensures the accurate recording of financial transactions and the faithful representation of the entity’s financial position in its financial statements.

- Consistency: Following a structured accounting cycle fosters consistency in financial reporting, facilitating comparisons of financial data across different time frames.

- Transparency: Well-documented and organized financial records enhance transparency, simplifying audits, compliance efforts, and earning the trust of stakeholders.

- Informed Decision-Making: Timely access to accurate financial information generated through the accounting cycle is imperative for effective decision-making by both management and external stakeholders.

Conclusion

The accounting cycle stands as a crucial process in the realm of finance and business. By adhering to these systematic steps, organizations can uphold dependable financial records, generate precise financial statements, and make well-informed decisions.

It serves as the bedrock of financial reporting and contributes to the transparency and credibility of an entity’s financial data, benefiting all stakeholders, both internal and external. Proficiency in comprehending and implementing the accounting cycle is essential for anyone engaged in financial management and reporting.